In financial terms, ‘risk’ is not having enough money to achieve your life priorities.

But it comes in different forms…

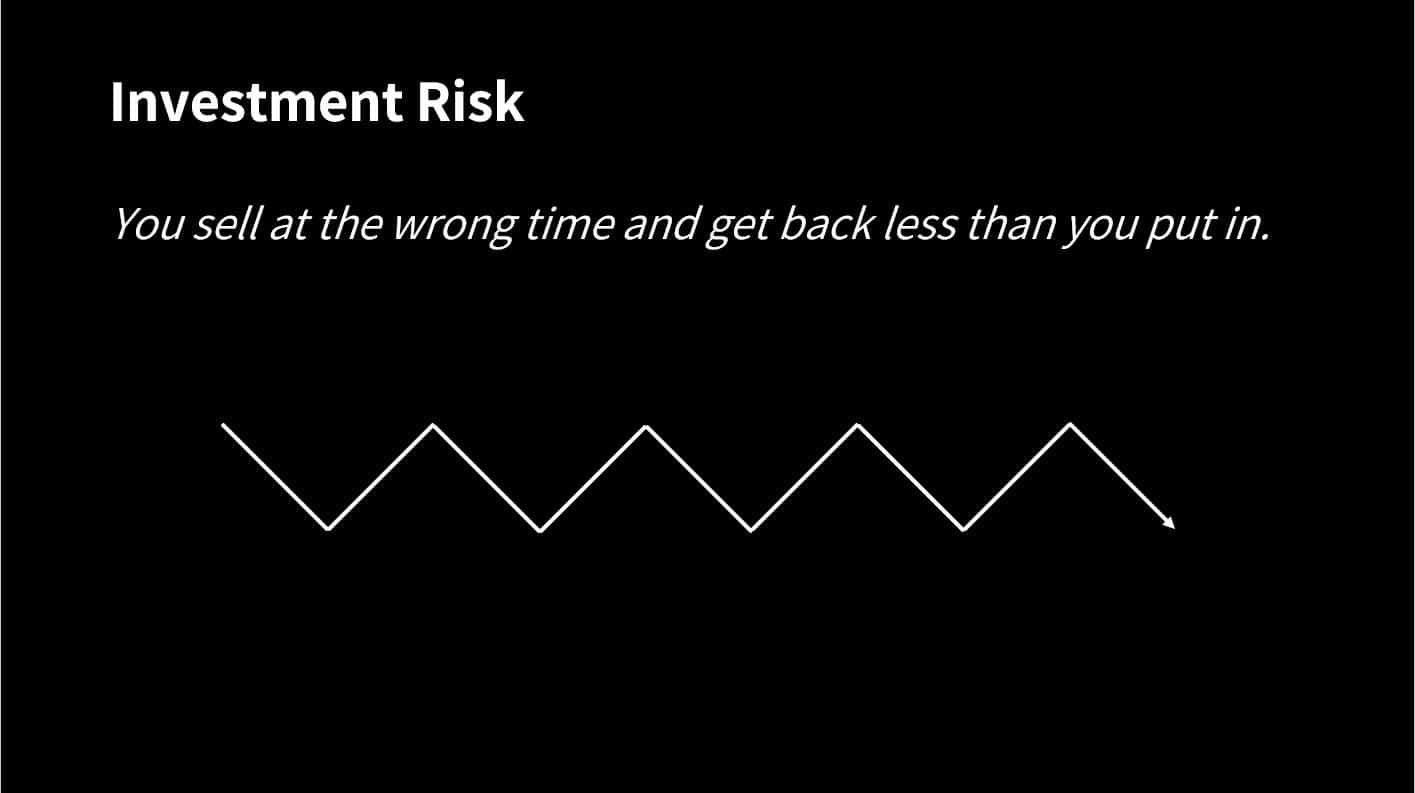

Investment Risk

Investment risk is what we most commonly associate with investing money. It is the risk that we get back less than we put in following stock market falls. It is measured in terms of volatility; the more volatile something is the greater the spread of returns.

A truism of investing is that if you want to receive higher returns you must accept a higher level of risk (and therefore the greater potential for losses). You can’t expect to have high returns without risk. Therefore if you don’t want to, or can’t afford to, take a risk with your money you have to accept lower returns, which brings us to inflation risk.

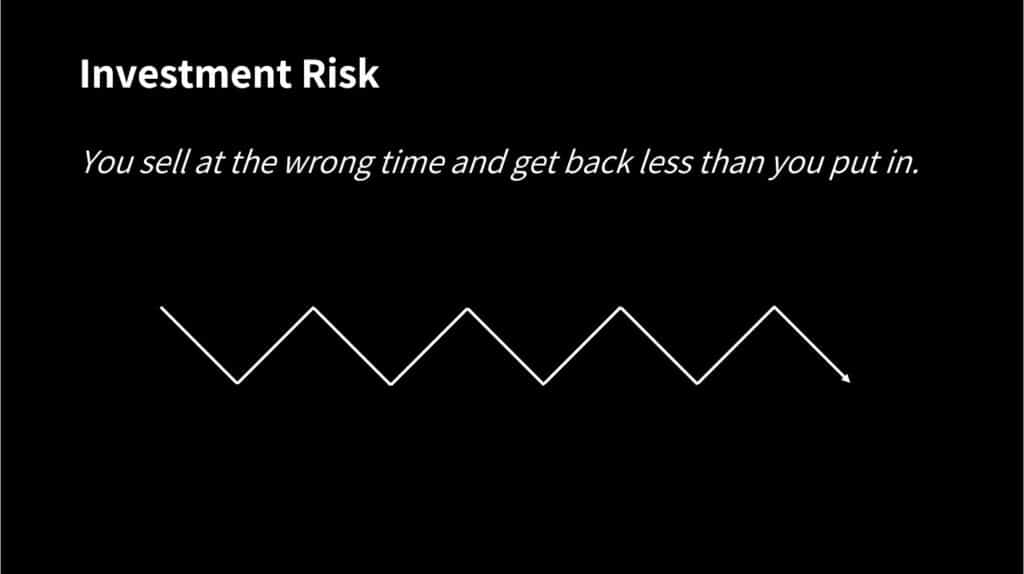

Inflation Risk

Inflation risk is the chance that the value of your money is eroded by inflation. Expressed another way, your money loses its purchasing power because as products and services get more expensive the value of your money isn’t increasing at the same rate.

The money you have in savings is exposed to inflation risk because the interest rates banks provide tend to be lower than the inflation rate. Even during times of rising interest rates, the net effect is the same because interest rates rise as a result of rising inflation (because central banks like the Bank of England raise the Base Rate in an attempt to cool rising inflation).

There is an irony that the risk-averse have all their money in savings for fear of losing it in the stock markets, but it is the unnoticeable effect of inflation that does more long-term damage than the stock markets.

That is not to say it’s inappropriate to have money in savings. It is wise to have an emergency fund to cover unforeseen expenses or periods of lost income but holding too much in savings will be detrimental to your long-term wealth. Which leads us to institutional risk.

Institutional Risk

Institutional risk is the risk that the company that we rely on to hold our money becomes insolvent, taking our money with it. The last time it was a severe problem was between 2007-2009 when the ‘Credit Crunch’ hit and forced many large banks and investment companies to fail (remember Northern Rock?). This lead to the central banks stepping in to bail many more out.

In the UK the Financial Services Compensation Scheme (FSCS) protects our savings in any single banking institution up to £85,000. Balances above this should be spread around several banks. For invested assets, the compensation scheme is less generous but there are different layers of safeguards should the investment firm holding our money fail.

Unforeseen Costs Risk

Life can have a habit of throwing the odd curve ball and when that happens there is usually a cost implication. As mentioned above, having money set aside in savings to act as an emergency fund is prudent. It means that if you have an expected bill such as for a car or house repair, to pay for private medical expenses or perhaps to help out children, money is available rather than having to borrow it at extra cost or raiding pensions and ISA investments that are set aside for longer-term priorities.

There is no set amount to have in an emergency fund but a helpful rule-of-thumb guide is to have 3-6 months’ worth of essential expenditure available.

Another part of this is the loss of income, perhaps due to redundancy, accident or illness that prevents you from being able to earn a living. The emergency fund can help plug this gap in the short-term but for more serious situations that result in longer periods out of work, potentially many years, establishing life assurance can protect against this risk.

Income protection policies pay out a regular monthly income for as long as the claimant is out of work suffering from a pre-defined illness or resulting from an accident. Critical Illness policies pay out a lump sum on the diagnosis of a specific illness. The lump sum can be used to pay off debt or make necessary home improvements that are required as a result of the illness.

Should the worse happen and loved ones will be financially exposed if you die, term assurance and family income benefit policies can pay out either a lump sum or regular income following your death.

Capital Risk

Any investment carries the risk of loss (see investment risk above), but some investments are riskier than others and could lead to a complete loss of capital. Investing in the shares of single companies is one such investment; if a company fails the shareholders have no claim when it goes into administration. This is why not having all of your eggs in one basket is sage advice.

An even greater risk is putting your money into something that seems too good to be true. Further sage advice is that if something seems too good to be true it probably is. Most likely the offer is a scam with no chance of any capital return whatsoever.

Currency Risk

Currency risk is the effect on your purchasing power of buying goods and services abroad. Whether you import or export products as part of a business, holiday abroad or invest in foreign companies within your pension or investment portfolio, the changing value of Sterling relative to currencies such as the US Dollar or Euro means that what you receive for your money can change daily.

This can work in your favour if the value of the pound strengthens against foreign currencies and you are buying goods and services abroad (because you need fewer pounds to buy the same amount) but it can also work against you when the pound weakens.

The effect works the other way if you are selling foreign investments to bring them back to the UK; a strong pound means you get less back on the exchange rate than when it is weaker. If your pension or investment fund is invested in overseas markets (which it probably is even if you are unaware), the fund managers tend to buy derivatives to offset this currency risk on your behalf.

Conclusion

Hopefully, having read this you can now see that there is more to risk than just the value of your investments falling. As stated at the start of this post, ‘risk’ should be seen as the chance of you not achieving your lifetime priorities. When you consider what you do with your money you should consider all these variations when coming up with a plan based on what you are trying to achieve and in what timeframe.

If you want assistance in coming up with a plan contact me to discuss it further.