If you do any background research on investing it won’t be long until you come across the term ‘Volatility’. Investment professionals and financial regulators use it to define investment risk but what do they mean by volatility and does it matter to you?

To get technical for a minute (and at the risk of reviving unwanted memories of your school maths lessons) volatility is measured by Standard Deviation. Or, put simply, how much a range of returns varies to the average of those returns.

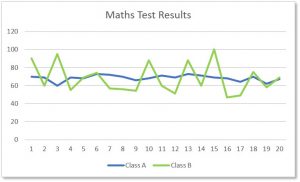

To give you an example, and while the memory of maths lessons may still be in your head, imagine maths test results from two different classes: the first class (Class A) is made of pupils of similar and high mathematical ability. The second class (Class B) has a much broader range of ability; some pupils are extremely good at maths, others struggle.

You can see from the chart below how the range of those test results varies. The average result of the two classes is the same (68%) but the range of class B is much greater. In other words, the standard deviation is higher (16.44 compared to 3.38).

Understanding the standard deviation in investing terms is helpful when comparing different investments, especially if you are uncomfortable seeing the value of your investment swing greatly on daily, monthly or yearly basis.

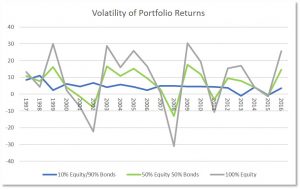

The chart below shows the range of returns of three different portfolios* with different allocations to equities (shares) over the past twenty years: 90% global equities & 10% global bonds; 50% global equities & 50% global bonds and 100% global equities. You can see that the range of returns widens the higher the equity allocation.

The 100% equity allocation has significant swings ranging from -31.1% in 2008 to +30.4% in 2009. As such the volatility as measured by Standard Deviation is much greater: 17.33 compared to 8.49 for the 50/50 mix and 2.67 for the 10% equity allocation.

However, investors are rewarded over the long-term for taking more investment risk. The average annual return of the 100% equity portfolio was 9% compared to 7% for the 50/50 portfolio and 4% for the 10% equity portfolio.

Given enough time the compounding effect of this small annual difference is substantial: a £100,000 investment over 20 years with a 2% pa outperformance equates to an extra £148,595 or an extra £265,330 for a 5% pa difference.

Time is the Greatest Healer

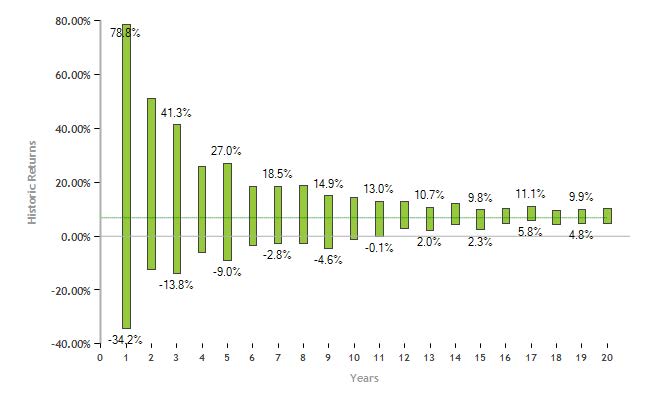

The principle of being rewarded for taking investment risk is a very important consideration for investors. In fact, volatility reduces over time as shown by this ‘corridor of returns’ chart** below.

It shows the range of returns for a high equity portfolio over twenty years. You can see that, based on historic returns, over one year the potential range of returns is very high (between -34.2% and 78.8%. A range of 113%) but over time that range reduces to 5.1% (rolling 20 year returns vary between 4.8% and 9.9% depending upon the start of the investment period).

In other words, time reduces volatility because we expect equity markets to provide positive long-term returns.

Volatility and Risk Are Not The Same Thing

Volatility and risk are often (usually) conflated but they are not the same thing.

‘Risk’ should not be seen only in terms of volatility. There are many different types of risk from inflation risk and institutional risk to currency risk. All of which are covered in this brief video.

Inflation is perhaps the silent killer of the risks because it is easily ignored but the long-term effects on wealth can be devasting. According to the Bank of England, the rate of inflation over the past 30 years (a likely length of retirement) was 3.3%. That means that £100,000 left in savings would only be worth £37,395 in 30 year’s time!

It is also important to consider ‘capacity for loss’ when investing any money. This is whether, as an investor, you can afford to suffer short-term declines in the value of a portfolio. If you have little income and are likely need to access capital in the short-term your capacity for loss is low (so the risk of investing in equities is greater).

Conversely, if you have high disposable income, from, say, a final salary pension, and have others savings so you don’t need to touch investment capital in the short-term, your capacity for loss is much higher.

Understanding risk in all its forms is especially important when deciding upon a strategy for income in retirement: too much risk and you may worry too much everytime there is a stock market correction and are more likely to make an irrational and regrettable decision. Too little and the combination of portfolio withdrawals and inflation may leave you with too much life at the end of the money.

So actually ‘risk’ and volatility are two different things. Assuming they are the same thing is risky in itself because it creates an opportunity cost. By not exposing capital to equity markets you are losing the opportunity to benefit from greater long-term returns that can be used for future discretionary expenditure; paying for the cost of later life care or gifted to the next generation in your lifetime or on death.

Indeed, the greatest risk you face is the risk of outliving your money. To avoid that you need to make sure your money is working appropriately for your unique situation.

If you would like to discuss how much investment risk is appropriate for your wealth contact me for an initial discussion.

Past performance is not a guide to the future. Future investment returns will differ from the past.

* Source EBI Portfolios Matrix Book Sept 2017. Returns are simulated where actual portfolio returns were not experienced.

** Source: Oxford Risk