When clients first start thinking about their pensions, the conversation can quickly result in jargon — defined benefit, money purchase, SIPPs, Final Salary and so on. That language is necessary, but it is often confusing.

Metaphors and analogies can help clarify complex topics. For pensions, the natural world offers a useful comparison.

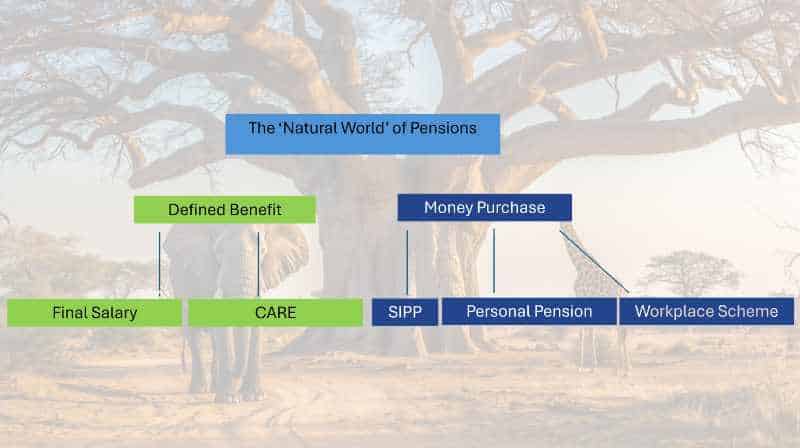

We all know the natural world consists of two kingdoms: plants and animals. We can also separate pensions into two ‘kingdoms’: Defined Benefit on one side, and Money Purchase on the other. Within each of these are different “species” with their own characteristics.

The Defined Benefit Kingdom: Predictable and Dependable

Defined Benefit (DB) pensions are like the stable giants of the plant kingdom. Imagine them as oak trees. With these pensions, what you earn in retirement isn’t down to investment performance or how much your pot has grown. Instead, it’s based on your salary and how long you’ve been a member of the scheme. In retirement, you receive a set fraction of your salary multiplied by your years of membership (‘service’).

We can divide the Defined Benefit kingdom into two sub-branches:

-

Final Salary Schemes – These are traditional schemes in which your pension is calculated based on your final (or near‑final) salary and years of service. The closer you get to retirement, the clearer your projected income becomes.

We can take the analogy further and characterise these pensions as critically endangered: they are increasingly rare, as employers, due to their high costs, close them to new members. If you have one, this guaranteed income stream is highly valuable.

-

CARE Schemes (Career Average Revalued Earnings) – In these schemes, your pension is based on your earnings across your career, rather than just at the end. Each year’s earnings are revalued (usually for inflation) and then added together to form your pension. As with Final Salary schemes, they give you a steady, reliable income in retirement, just not based on your salary when you leave the scheme, which is typically higher at the end of your career.

Public sector schemes such as the NHS, LGPS, and Teachers’ Pension run CARE schemes. If you’ve worked for long periods, you may be a member of both types, each with a different retirement age.

Both types give you certainty, which is why many people approaching retirement hold onto them tightly.

The Money Purchase Kingdom: Flexible and Growth‑Oriented

The other branch of the pension world is Money Purchase pensions. These do not offer a guaranteed income. The size of your pension pot and the income you get in retirement depends on contributions made, investment returns, charges and how long you leave the money invested.

Within this kingdom you’ll typically find:

-

Personal Pensions – These are the straightforward pensions which may have been set up by you or a former employer. You will have made a decision about how to invest the money (many investors accepted the default option, which may no longer be appropriate), made contributions and left it to grow. There are thousands of small pots, often forgotten about, that received contracted out or SERPS rebates decades ago.

-

SIPPs (Self‑Invested Personal Pensions) – These are more modern pensions and tend to be offered by direct to investor platforms. They aim to give you a lot of choice about where you invest; you can choose from a wide range of investment options, including direct shares, funds and commercial property. However, many investors end up paying for a level of choice they neither use nor need.

-

Workplace Pensions (DC schemes) – Since auto‑enrolment was introduced in 2012, most employees will have joined their employers’ pension scheme by default. They are fairly basic in design with limited investment options and flexibility at retirement. They aim to do a simple job: you and your employer contribute prescribed minimum amounts, and the money is usually invested in a default fund that aims to suit people saving for retirement. NEST and the People’s Pension are two of the biggest workplace pension providers.

Why These Differences Matter

Understanding which “kingdom” your pension sits in is important because it affects how you plan for retirement.

A Defined Benefit pension gives you something very powerful: certainty. In retirement, you receive a set amount each month, which usually increases each year in line with inflation and provides a spouse’s income on death. Market performance becomes irrelevant.

To continue the analogy, Money Purchase pensions are more like managing animals; you need to feed them (make contributions)), where they roam (investment strategy), and how to make sure they stay healthy (managing risk and charges). They offer flexibility but require more decision‑making.

Nowadays, many people approaching retirement will have a mix. But if you worked in the public sector for your entire career, you are likely to have just a defined benefit pension. Whereas, the self-employed may be reliant on contributions they have made to a personal pension. For anyone starting their career now, Defined Benefit pensions may feel like dinosaurs; their pension savings are likely to be a series of workplace pensions.

Using This to Plan Better

Here’s the practical bit. As you approach your retirement:

-

Know what you’ve got. Take time to understand which pensions you hold, what type they are and what you can realistically expect from them.

-

Value guaranteed income. If you have a DB scheme, treat that as a cornerstone of your income in retirement. It’s predictable and hard to replicate with a Money Purchase pot.

-

Care for your Money Purchase pots. Pay attention to how they’re invested and what charges you’re paying. Over time, investment choices and fees can significantly impact the size of your pot.

-

Think long term. Unlike the plant and animal kingdoms, your pension doesn’t just fend for itself. Your choices, whether made with professional support or through careful personal planning, will shape how well it sustains you in retirement.

At its heart, planning for retirement is about giving you the confidence to enjoy the life you want when you stop working. Understanding what you have is an essential step in having security and choice.

If you’d like to talk about how your pensions fit together and what that means for your retirement, don’t hesitate to get in touch.

Andrew Neligan is a retirement financial planner in East Devon who helps individuals and couples in their 50s and early 60s plan their transition into retirement and create sustainable retirement income