Knowledge is power. In investing terms that means uncovering a gem of information that gives the investor an advantage against his peers in predicting the future direction of company share prices, a sector, market or an asset class.

If information comes to light that is an opportunity or threat to a particular investment the insightful investor can act on it to benefit from the fall or gain in the share price once that information becomes more widely available.

The problem for investors, be they professionals or amateurs is that technology has levelled the playing field and devolved the power that comes from knowledge from the few to the many. In other words, millions of investors, traders and speculators the world over have access to the same information on which to predict future returns.

Thinking Collectively

A share’s price is the result of the aggregate assessment of the potential return for that share based upon the available information relating directly and indirectly to that company at any point in time. Owning shares in a company comes at a risk (the risk the company becomes insolvent) so investors expect the reward of an increasing share price and a regular dividend income to offset that risk.

If there are a greater number of investors who are pessimistic about the company’s fortunes (and therefore the financial reward for taking the risk of holding the company’s shares is low or negative), the share price will fall (and vice versa when the outlook is positive and there are more buyers than sellers, at which point the share price will rise).

The share price is, therefore, the fair reflection on the aggregate view of all market participants. It might not be correct but it is as fair and efficient as it can be. Because there are trillions of dollars in shares traded daily it can’t be anything other than a fair reflection of the average view of all investors.

The value of any index, such as the FTSE100 or the S&P500 in the US, is, therefore, the aggregate value of all shares within the index and must represent a fair reflection of the market participants expectations of the sum of the companies in that index on any given day (or more accurately, second).

Using the Rugby World Cup As an Example

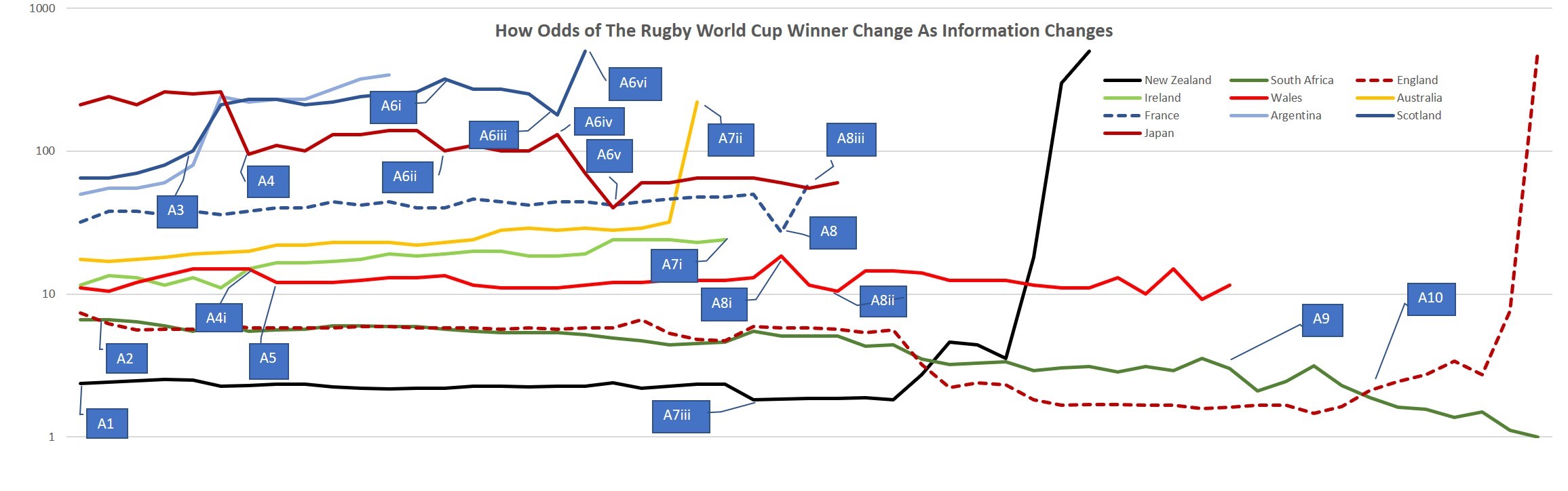

It is only when new information comes to light that the value of a share (and therefore market) will change. To explain this in non-financial terms I have logged the odds on the winner of the Rugby World Cup over the past 6 weeks from a popular betting exchange*.

The fact that I have used a betting exchange rather than a bookmaker is important because the betting exchanges represent the views of many individuals betting against each other, much like a stock market. It is also a live market with odds changing during a match to demonstrate how changes within a match affect the odds of each team winning and losing.

You can see from the chart below how the odds increase and decrease as the perceived chance of each nation winning the world cup changes when new information is made available. If you are not familiar with how odds on a betting exchange work, the smaller the number the greater the expectation is of winning (i.e. the odds are lower)

(click to view larger image)

(click to view larger image)

For example:

- New Zealand starts as clear favourites (A1).

- England’s odds of winning improve when they beat Ireland (another tournament favourite) in a warm-up game (A2).

- The odds of Argentina and Scotland worsen on the build-up to the tournament following poor warm-up results. The odds increase further following defeats in the opening matches (A3).

- The first upset of the tournament is when the hosts Japan beat Ireland. Japan’s odds of winning improve (A4) while Ireland’s worsen (A4i)

- Wales beat another tournament favourite, Australia, in the pool matches so their odds improve (A5)

- A good example of how external events can affect expectations is when typhoon Hagibis threatened to cancel Scotland’s crunch game with Japan. Cancellation would have sent Scotland home and secured Japan’s qualification to the knockout stages. Scotland’s odds lengthened (A6i) as Japan’s shortened (A6ii).

- The game ended up going ahead meaning Scotland still had a chance to progress and Japan could still have been knocked out at the pool stage so Scotland’s odds improved slightly (A6iii) and Japan’s dropped (A6iv). In the end, Japan won the match and qualified so their odds improved dramatically (A6v) but Scotland crashed out of the tournament (A6vi).

- In the knockout stages, Ireland lost to New Zealand (A7i) and Australia lost to England so both countries’ World Cup’s came to an end. New Zealand, already the overwhelming favourites to win the tournament, saw their odds improve due to the strength of their performance against Ireland (A7iii)

- The Wales versus France quarter-final is an interesting one; France were leading Wales at half time so their odds improved (A8) but Wales’ expected chances of winning the tournament decreased (A8i). However, Wales eventually beat France so their odds improved significantly (A8ii) and France went home (A8iii)

- Another notable point is that the odds of each country winning fluctuate over time regardless of any particular event occurring that might have a positive or negative impact on them winning the tournament. As with fluctuations in a company’s share price, there is always an element of market ‘noise’ that sees odds or share prices change slightly. There is no new significant information but prices change all the time.

- South Africa’s odds of winning trend down as they progress to the final and ultimately win (A9).

- England’s odds improve on route to the final but then lengthen as South Africa dominate the final (A10).

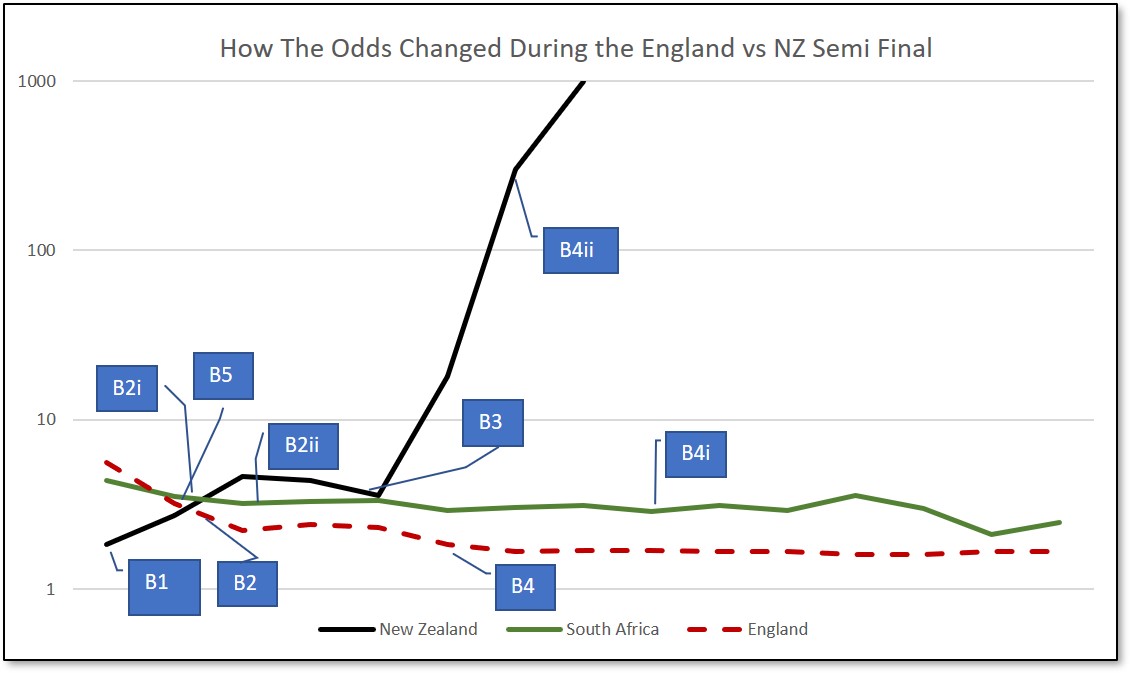

The next chart below shows how odds change quickly within a game as the scoreline fluctuates.

- On the eve of the semi-final between England and New Zealand, New Zealand were still the overwhelming favourites to win the game and the tournament (B1)

- However, England scored early and were leading at half-time so their odds improved with their prospects of winning the game and with it the World Cup (B2). This meant the chance of New Zealand winning the tournament reduced (B2i).

- Also, notably, with New Zealand looking like they might go home, the second-favourites to win the tournament, South Africa, saw their odds improve as a result (B2ii).

- When New Zealand scored to reduce England’s lead their odds improved slightly (B3) whilst England’s and South Africa’s dipped marginally.

- However, England kept scoring, improving their odds (B4) and those of South Africa (B4i) while New Zealand’s odds kept lengthening as time ran out on them (B4ii).

- Furthermore, such was the dominance of England’s performance over the tournament favourites, they became the overall favourites, ahead of South Africa (B5), who had been second-favourites from the build-up to the tournament, right up to half-time of that game.

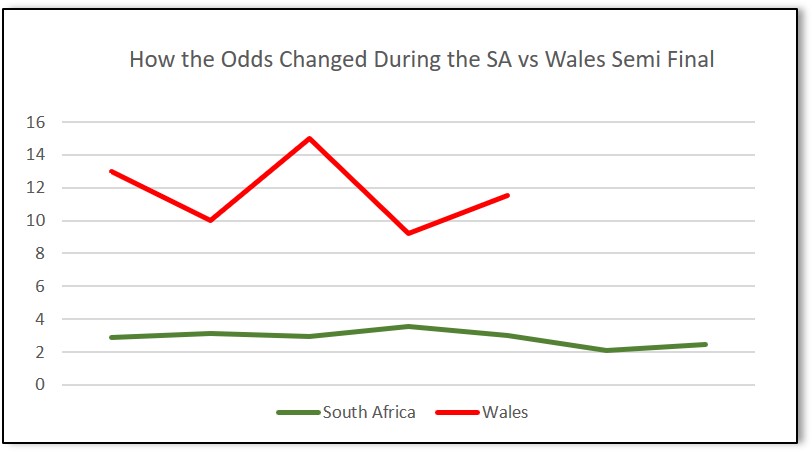

The third chart below focuses on the Wales versus South Africa semi-final which was a much closer game with the South African’s taking the lead a couple of times only for Wales to level the scores again. Notice how the odds fluctuate accordingly until South Africa stretch the lead and ultimately win.

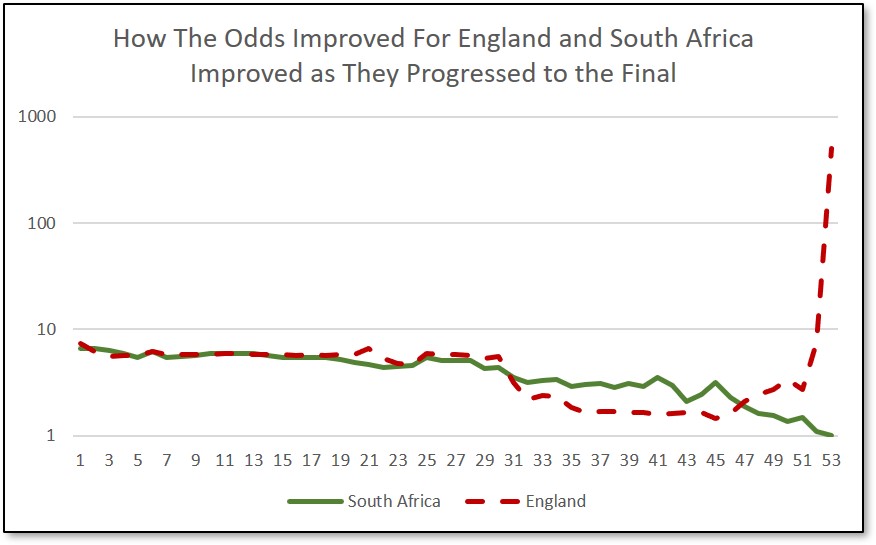

The chart below shows an overview of how the odds of both England and South Africa winning the tournament improved as they progressed through the tournament until, from England’s point of view, the scoreline got too far away from them and the loss was inevitable.

I

Bringing it Back to Shares

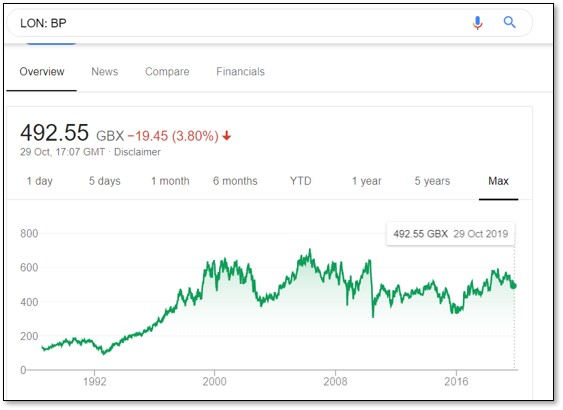

To bring it back to the investment world and to demonstrate how a company’s share price changes as new information become available, the chart below, taken from Google Finance, shows the long-term return of BP’s share price.

You can see how the price ticked up progressively during the 1990s until it took a big hit, along with the rest of the market in 2002/03 (this is what economists call ‘systematic risk’ because it affects the whole market).

The share price recovered, along with the rest of the market during the noughties until the Great Financial Crash of ’08/’09 (systematic risk again).

The biggest event to affect BP’s share price, however, was company-specific (unsystematic risk). In 2010 there was an explosion on BP’s drilling platform, Deep Water Horizon, that killed many and caused untold environmental damage. The handling of the situation by BP’s executives in the aftermath was a disaster and the share price has not yet recovered from the financial and non-financial fall out of that catastrophe.

Conclusion

The message to take away from this post is that there are so many variables and unknowns that affect market prices (or an outcome of a sporting fixture) and so many market participants that it is very difficult, if not impossible, for any single investor to advantage from unique insights.

If you are paying extra for an active fund manager to access their ‘unique insights’ you are most likely better to save your money and simply follow an index and accept the ups and downs that come from stock market investing.

Furthermore, the systematic (market) risk is an ever-present and must be accepted if you want higher, longer-term returns. Unsystematic risk, on the overhand, is avoidable by diversifying a portfolio within and across stock markets. Doing so prevents any single holding, such as BP, destroying your financial plan.

If you would like to discuss your investment requirements please do not hesitate to get in touch. You can do so by clicking here.

*Prices are taken from Betfair Exchange. Other betting exchanges are available. The use of Betfair’s prices is not an endorsement of the exchange specifically and betting generally.

Photo by Thomas Serer on Unsplash